Intel Reports Q3 2021 Earnings: Client Down, Data Center and IoT Up

Kicking off another earnings season, Intel is once again leading the pack of semiconductor companies in reporting their earnings for the most recent quarter. As the company gets ready to go into the holiday quarter, they are coming off what’s largely been a quiet quarter for the chip maker, as Intel didn’t launch any major products in Q3. Instead, Intel’s most recent quarter has been driven by ongoing sales of existing products, with most of Intel’s business segments seeing broad recoveries or other forms of growth in the last year.

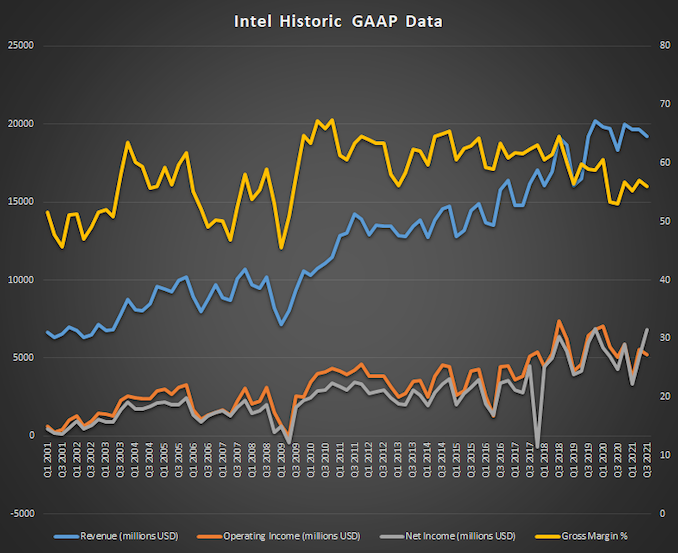

For the third quarter of 2021, Intel reported $19.2B in revenue, a $900M improvement over the year-ago quarter. Intel’s profitability has also continued to grow – even faster than overall revenues – with Intel booking $6.8B in net income for the quarter, dwarfing Q3’2020’s “mere” $4.3B. Unsurprisingly, that net income growth has been fueled in part by higher gross margins; Intel’s overall gross margin for the quarter was 56%, up nearly 3 percentage points from last year.

| Intel Q3 2021 Financial Results (GAAP) | |||||

| Q3’2021 | Q2’2021 | Q3’2020 | |||

| Revenue | $19.2B | $19.7B | $18.3B | ||

| Operating Income | $5.2B | $5.7B | $5.1B | ||

| Net Income | $6.8B | $5.1B | $4.3B | ||

| Gross Margin | 56.0% | 53.3% | 53.1% | ||

| Client Computing Group Revenue | $9.7B | -4% | -2% | ||

| Data Center Group Revenue | $6.5B | flat | +10% | ||

| Internet of Things Group Revenue | $1.0B | +2% | +54% | ||

| Mobileye Revenue | $326M | flat | +39% | ||

| Non-Volatile Memory Solutions Group | $1.1B | flat | -4% | ||

| Programmable Solutions Group | $478M | -2% | +16% | ||

Breaking things down by Intel’s individual business groups, most of Intel’s groups have enjoyed significant growth over the year-ago quarter. The only groups not to report gains are Intel’s Client Computing Group (though this is their largest group) and their Non-Volatile Memory Solutions Group, which Intel is in the process of selling to SK Hynix.

Starting with the CCG then, Intel’s core group is unfortunately also the only one struggling to grow right now. With $9.7B in revenue, it’s down just 2% from Q3’2020, but that’s something that stands out when Intel’s other groups are doing so well. Further breaking down the numbers, platform revenue overall is actually up 2% on the year, but non-platform revenue – “adjacencies” as Intel terms them, such as their modem and wireless communications product lines – are down significantly. On the whole this isn’t too surprising since Intel is in the process of winding down its modem business anyhow as part of that sale to Apple, but it’s an extra drag that Intel could do without.

The bigger thorn in Intel’s side at the moment, according to the company, is the ongoing chip crunch, which has limited laptop sales. With Intel’s OEM partners unable to source enough components to build as many laptops as they’d like, it has the knock-on effect of reducing their CPU orders, even though Intel itself doesn’t seem to be having production issues. The upshot, at least, is that desktop sales are up significantly versus the year-ago quarter, and that average selling prices (ASPs) for both desktop and notebook chips are up.

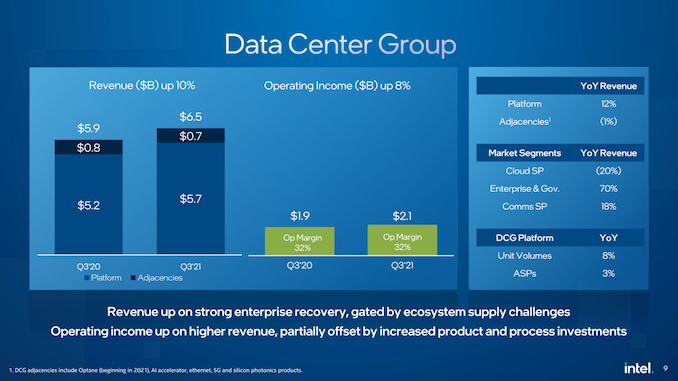

Meanwhile, Intel’s Data Center Group is enjoying a recovery in enterprise spending, pushing revenues higher. DCG’s revenue grew 10% year-over-year, with both sales volume and ASPs increasing by several percent on the back of their Ice Lake Xeon processors. A bit more surprising here is that Intel believes they could be doing even better if not for the chip crunch; higher margin products like servers are typically not impacted as much by these sorts of shortages, since server makers have the means to pay for priority.

Unfortunately, unlike Q2 Intel isn’t providing a quarter-over-quarter (i.e. vs the previous quarter) figures for their earnings presentation. So while overall DCG revenue is flat on a quarterly basis, it sounds like Intel hasn’t really recovered from the hit they took in Q2. Meanwhile, commerntary on Intel’s earnings call suggests the sales of the largest (XCC) Ice Lake Xeons has been softer than Intel first expected, which has kept ASP growth down in an otherwise DCG-centric quarter.

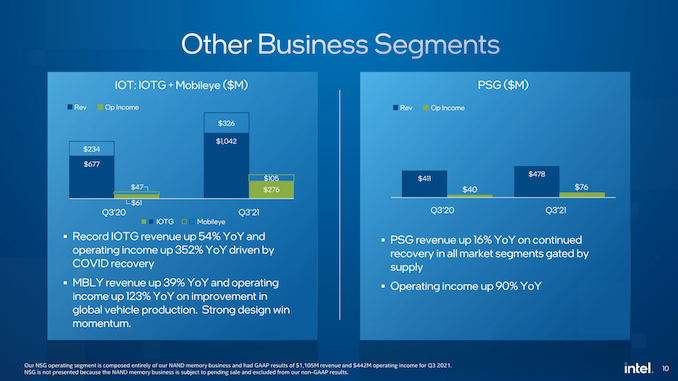

The third quarter was also kind to Intel’s IoT groups and their Programmable Solutions Group. All three groups are up by double-digit percentages on a YoY basis, particularly the Internet of Things Group (IoTG), which is up 54%. According to Intel, that IOTG growth is largely due to businesses recovering from the pandemic, with a similar story for the Mobileye group thanks to automotive production having ramped back up versus its 2020 lows.

Otherwise, Intel’s final group, the Non-Volatile Memory Solutions Group, was the other declining group for the quarter. At this point Intel has officially excised the group’s figures from their non-GAAP reporting, and while they’re still required to report those figures in GAAP reports, they aren’t further commenting on a business that will soon no longer be theirs.

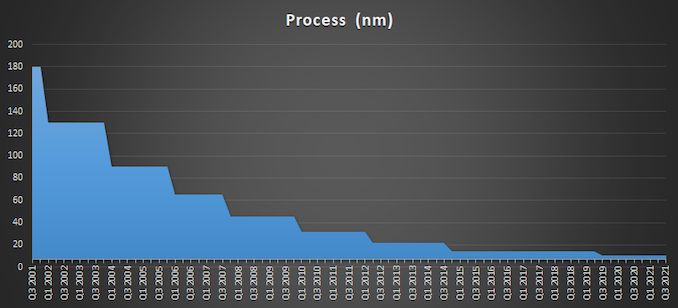

Finally, tucked inside Intel’s presentation deck is an interesting note: Intel Foundry Services (IFS) has shipped its first revenue wafers. Intel is, of course, betting heavily on IFS becoming a cornerstone of its overall chip-making business in the future as part of its IDM 2.0 strategy, so shipping customers’ chips for revenue is an important first step in that process. Intel has laid out a very aggressive process roadmap leading up to 20A in 2024, and IFS’s success will hinge on whether they can hit those manufacture ring technology targets.

For Intel, Q3’2021 was overall a decent quarter for the group – though what’s decent is relative. With the DCG, IOTG, and Mobileye groups all setting revenue records for the quarter (and for IOTG, overall records), Intel continues to grow. On the flip side, however, Intel missed their own revenue projections for the quarter by around $100M, so in that respect they’ve come in below where they intended to be. And judging from the 7% drop in the stock price during after-hours trading, investors are taking note.

Looking forward, Intel is going into the all-important Q4 holiday sales period, typically their biggest quarter of the year. At this point the company is projecting that it will book $18.3B in non-GAAP revenue (excluding NSG), which would be a decline of 5% versus Q4’2020. Similarly, the company is expecting gross margins to come back down a bit, forecasting a 53.5% margin for the quarter. On the product front, Q4 will see the launch of the company’s Alder Lake family of processors, though initial CPU launches and their relatively low volumes tend not to move the needle too much.

On that note, Intel’s Innovation event is scheduled to take place next week, on the 27th and 28th. The two day event is a successor-of-sorts to Intel’s IDF program, and we should find out more about the Alder Lake architecture and Intel’s specific product plans at that time.

Source: Recent News